India’s fintech story of the last decade was written in unsecured credit — instant personal loans, buy-now-pay-later checkouts, and app-based lines of credit that reached millions of first-time borrowers. But a quieter opportunity has been sitting in plain sight: the vast pool of assets Indian households and businesses already own, most of which never gets converted into usable credit. Bengaluru’s Spense wants to build the plumbing for exactly that — and a marquee list of backers has just written the first big cheque.

The raise

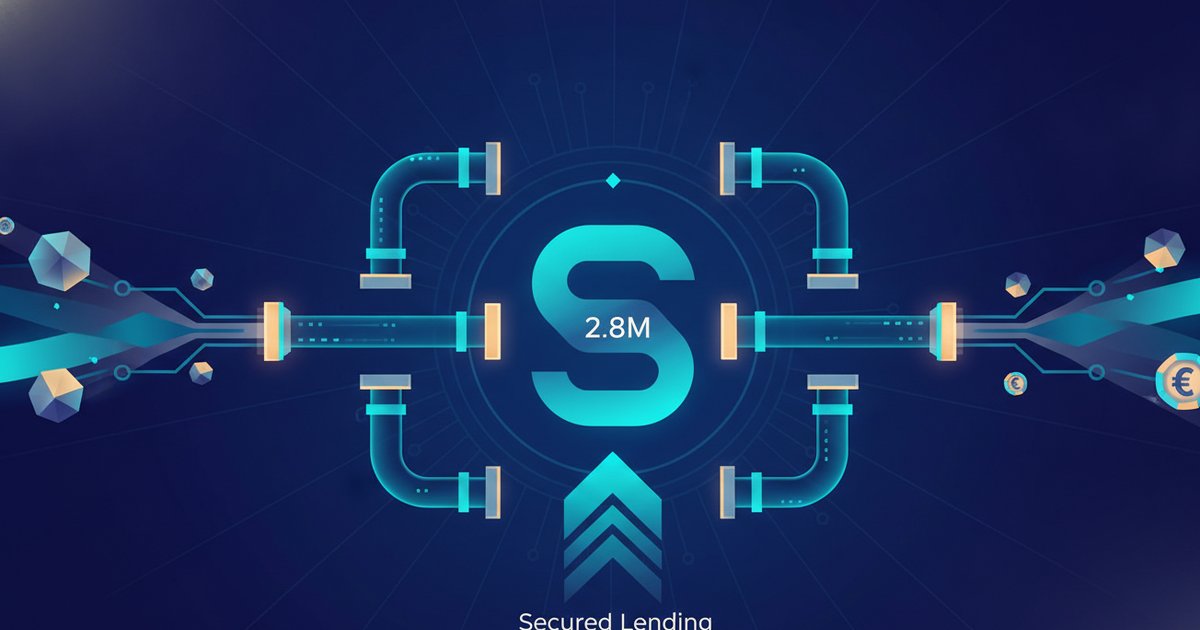

Spense has raised $2.8 million in seed funding led by Arkam Ventures, with Razorpay Ventures, Atrium Ventures and GrowthCap Ventures participating, according to a report in Indian Startup Times (July 1, 2026). GrowthCap is a continuing backer, having also participated in the company’s earlier pre-seed round — a signal of conviction from investors who have watched the team since its earliest days.

The round is notable as much for its angel roster as its institutional leads. Kunal Shah, the founder of CRED, and Madhusudhan E, co-founder of KreditBee, are among the fintech operators who put money in. That’s a who’s-who of people who have built consumer-credit and lending businesses at scale in India, and their presence reads as a bet on the category as much as the company. When the people who built the last generation of Indian lending rails back the next one, it’s worth paying attention to what they think is missing.

As always with early-stage rounds, the details here rest on single-source reporting, so specifics should be treated as indicative rather than fully confirmed. What’s clear is the shape of the thesis the money is chasing.

The thesis

Spense’s founding argument is a reframe. Most credit conversations in India start with risk — who will default, how do you price that risk, how do you recover. Spense instead treats credit as an infrastructure problem. Per Indian Startup Times, the founder has argued that India’s credit gap is less about risk appetite and more about missing rails: the country simply lacks the connective tissue to convert existing assets into usable credit.

That distinction matters. A risk-first framing pushes lenders toward tighter filters and higher prices. An infrastructure-first framing asks a different question: if a borrower already owns something of value — a fixed deposit, mutual fund units, gold, insurance, equity — why is it so hard, slow, and manual to borrow against it? The answer, more often than not, is plumbing. The asset sits with one custodian, the lender sits somewhere else, the lien-marking is clunky, and the verification is a paper trail. The value exists; the pipe to move it doesn’t.

The company’s stated view is that the future of banking will be shaped by two forces working together: asset-unlocking infrastructure that makes collateral programmatically usable, and AI-driven intelligence that makes underwriting faster and sharper. In practice, that points toward credit embedded directly into digital payment and financial flows — so that borrowing against an asset feels less like a loan application and more like a feature that’s simply available when you need it. The ambition is to make secured credit as frictionless as the unsecured variety has become.

Why secured lending now

India’s retail credit boom leaned heavily unsecured for good reasons. Unsecured lending scales fast: no collateral to verify, no lien to mark, no asset to seize. Digital-first lenders could underwrite on cash-flow and bureau data, disburse in minutes, and reach borrowers banks ignored. But that model has limits — and, over the past couple of years, regulators and lenders alike have grown more cautious about unsecured growth, stress in small-ticket loans, and the concentration risk of a book with nothing behind it.

Secured lending is the natural counterweight, and the timing is improving for three reasons.

- Asset-unlocking rails are maturing. India now has the digital public infrastructure — from account aggregators to digitised depositories and demat systems — that makes it possible to verify and pledge financial assets programmatically rather than through branch visits and physical paperwork. The rails Spense wants to build sit on top of this foundation.

- AI-led underwriting narrows the cost gap. The historic knock on secured lending was operational drag: valuation, verification, monitoring and recovery all cost money. Better data pipes plus AI-driven intelligence can compress that cost, letting lenders offer smaller, faster secured loans that were previously uneconomic.

- Lenders want quality collateral. After a cycle of unsecured stress, a loan backed by a liquid, easily-recoverable asset looks attractive. Lower loss-given-default can mean lower rates for borrowers and healthier books for lenders — a rare win on both sides.

None of this erases the hard parts. Secured lending trades one set of problems for another: collateral has to be valued accurately and monitored as its price moves, liens have to be enforceable, and recovery has to actually work when a borrower defaults. Market-linked collateral like equities or mutual funds introduces volatility that requires margin calls and real-time monitoring — infrastructure problems in their own right. The pitch is compelling precisely because these are unglamorous, plumbing-level challenges that a purpose-built infrastructure layer is well-positioned to solve, rather than something every lender should rebuild alone.

The India read

For the broader Indian fintech stack, Spense’s raise fits a recognisable pattern: the next layer of value is being built beneath the consumer app, not on top of it. The first wave digitised payments (UPI). The second wave digitised unsecured credit distribution. A plausible third wave is digitising collateral itself — turning under-used assets into a live, borrowable balance sheet that any lender or platform can plug into.

Done well, this deepens formal credit access in a way unsecured lending can’t fully reach. Households sitting on gold or a fixed deposit, and small businesses with equipment or receivables, could borrow against what they own at fairer prices than an unsecured line would offer — and without liquidating assets they’d rather keep. That’s a meaningful expansion of the formal credit perimeter, and it aligns with the direction Indian financial regulators have signalled they prefer: growth backed by real security.

For founders building in lending infrastructure, a few things are worth watching:

- Regulatory posture on collateral and recovery. Secured lending lives and dies on enforceability. Any friction in lien-marking, pledge and recovery frameworks directly shapes what’s economically viable.

- Distribution over origination. Infrastructure players win by being embedded everywhere — inside payment apps, neobanks and platform ecosystems — rather than by owning the customer. Spense’s embedded-credit framing suggests it understands this.

- Whether AI underwriting holds up through a cycle. Faster, cheaper underwriting is only an advantage if the models are sound when asset prices fall and defaults rise. The real test comes in a downturn, not a bull run.

- The unit economics of small-ticket secured loans. The prize is making tiny secured loans profitable. If the cost of verification, monitoring and recovery stays low enough, the addressable market is enormous.

India, by Spense’s own framing, does not lack assets. It lacks the plumbing. Whether this particular team builds the definitive rails is an open question, but the direction of travel is hard to argue with. The unsecured boom proved that Indians will borrow at scale when it’s easy. The next chapter may prove they’ll borrow better — and cheaper — when the assets they already own are finally put to work.