The story investors tell themselves about the next year is rarely about a single stock. It is about the price of money. And over roughly the last ten months, that story has been rewritten so completely that it is worth pausing to register the scale of the shift. Markets that once confidently priced a steady glide path of rate cuts are now bracing for the opposite. When the cost of capital moves that far, that fast, the assets most sensitive to it move with it — and few assets are more sensitive than the long-duration bet that is artificial intelligence.

This week’s AI-stock whiplash has been narrated as a story about chips, capex, and circular financing. Some of that is real. But the deeper current running underneath is monetary. To understand why high-quality AI names can fall several percent on a quiet news day, you have to look at what has happened to interest-rate expectations — and at what the Federal Reserve has stopped promising.

The Flip

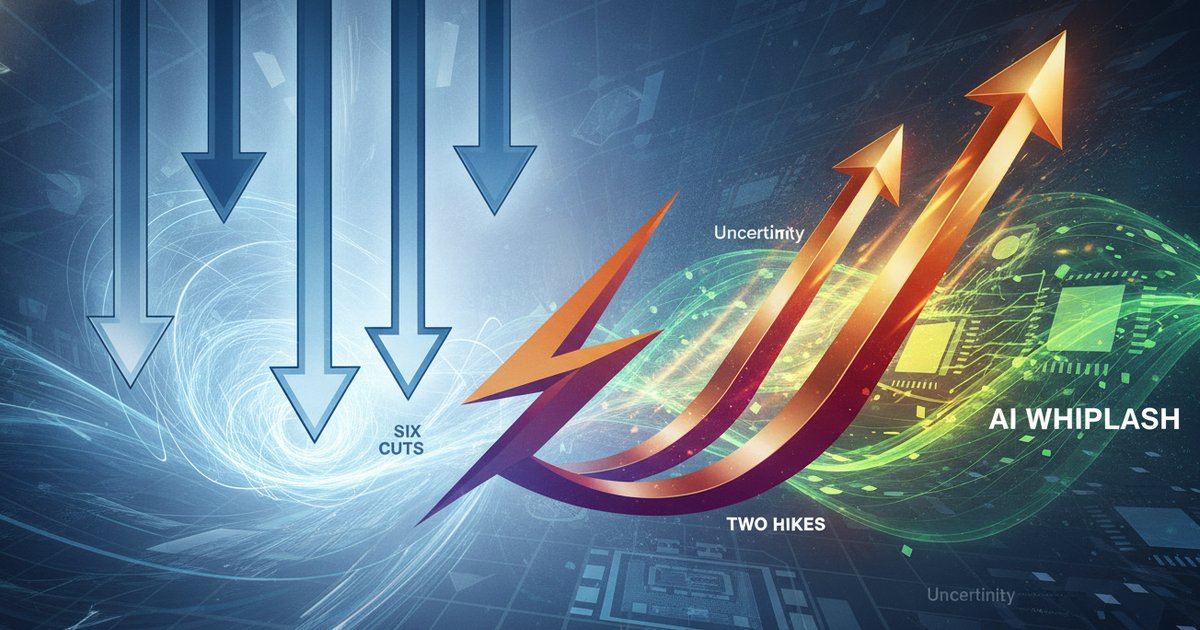

The reversal is the headline. According to coverage from Investing.com in late June 2026, markets have swung from pricing in a series of rate cuts to bracing for as many as two hikes over the span of about ten months. That is not a tweak to the forecast; it is a wholesale inversion of the direction of travel. An investor who built a portfolio around “rates are coming down, so reach for duration” has spent the better part of a year watching the foundation of that thesis dissolve.

What drove the change? Inflation refused to behave. The Fed’s preferred gauge — core PCE — posted its highest annual rise in some time as of late June 2026, per the same Investing.com reporting, which is worth verifying against the Bureau of Economic Analysis source data. The point is directional and clear: disinflation, which markets had treated as a settled trend, began to wobble. Reacceleration, even modest, is enough to force a repricing because it changes the entire conditional logic of policy.

Energy added a second push. PwC’s US Capital Markets Watch for the first quarter of 2026 notes that geopolitical pressure on Middle East energy flows pushed fuel prices higher, layering fresh uncertainty onto the inflation picture. Oil is one of the few inputs that feeds simultaneously into transport, manufacturing, and consumer expectations — which makes a sustained climb in crude particularly awkward for a central bank trying to declare victory. The same PwC review records that the Fed had already delivered around 75 basis points of cuts late last year before pivoting to a more patient stance. That pivot, in hindsight, was the hinge. The cuts had begun; then the data argued for waiting; and waiting, in a reaccelerating environment, started to look like it might mean reversing.

Why Rates Hit AI Hardest

If rates are rising across the board, why does the pain concentrate in AI? The answer is duration, and it is worth being precise about it.

The value of any company is, in theory, the present value of its future cash flows. For mature, cash-generative businesses, a large share of those cash flows arrive soon. For AI-leveraged growth names, the opposite is true: a disproportionate share of the expected value sits years out, in profits that have not yet materialized and business models that are still being proven. That makes them long-duration assets, in the same way a 30-year bond is more rate-sensitive than a two-year note. When the discount rate rises, you are discounting those distant cash flows more harshly — and the further out the cash flow, the more its present value shrinks. A move in rates that nicks a steady dividend payer can gut the implied valuation of a story stock whose payoff lives in 2030.

The second channel is capital expenditure. The AI build-out is extraordinarily capital-intensive — data centres, accelerators, power, and the financing arrangements stitched around them. A meaningful slice of that spending is debt-funded or depends on cheap capital staying cheap. When borrowing costs rise, every marginal gigawatt of compute gets more expensive to finance, the hurdle rate for new projects climbs, and the elegant math of “spend now, harvest later” gets less elegant. Investors who were happy to underwrite aggressive capex when money was free start asking harder questions when money is not.

Put the two together and you get the compression mechanic. Higher discount rates pull valuations down directly; pricier capex pressures the future cash flows those valuations rest on. The result is that AI stocks behave less like a sector and more like a leveraged bet on the rate path itself. This is the honest read on the whiplash: much of it is not a verdict on the technology. It is the market re-solving an equation in which the discount rate just changed.

The Honest Uncertainty

Here is where commentary usually overreaches, and where it should not. The Fed has not committed to hikes. It has committed to being data-dependent — which is a genuinely different thing, however unsatisfying that is for anyone who wants a clean forecast.

A data-dependent central bank is not following a fixed path; it is reacting to incoming numbers, meeting by meeting. That means the “two hikes” the market is now bracing for are a probability-weighted fear, not a scheduled event. If inflation prints soften and energy prices stabilize, the same data-dependence that produced hawkish pricing can swing back toward patience or even renewed cuts. The market’s job is to price the distribution of outcomes, and right now that distribution has simply shifted hawkish.

The core tension the Fed is managing is the classic one: growth versus inflation. Hike too hard to crush prices and you risk choking activity and employment; stay too loose and you let inflation expectations un-anchor. There is no costless choice, only a trade-off being managed in real time under incomplete information.

So what could change the call? A few things, and it is worth naming them honestly rather than pretending to know which wins:

- A clear, sustained downturn in core PCE that confirms reacceleration was a blip rather than a trend.

- Energy prices easing as geopolitical pressure on supply routes recedes, removing a key source of inflation uncertainty.

- Labour-market softening that tilts the trade-off back toward growth and gives the Fed room to cut.

- Conversely, sticky services inflation or another energy shock that hardens the hawkish case.

The intellectually honest position is to hold these scenarios simultaneously and size risk accordingly — not to pick one and bet the portfolio on it.

The Emerging-Market Read

For Indian founders, marketers, and operators, the relevant question is how all of this travels east. The transmission mechanism is capital flows. When US rates rise and the dollar firms, global capital tends to rotate toward dollar assets, where it can earn more for less risk. That pulls money out of emerging markets, pressures the rupee, and tightens domestic financial conditions even when the Reserve Bank of India has done nothing.

The spillovers are concrete. A weaker rupee makes imported energy — already climbing — more expensive in local terms, which can import inflation at exactly the wrong moment. Foreign portfolio outflows can weigh on Indian equities, and the richly valued, growth-heavy corners of the market are vulnerable to the same duration math punishing AI names abroad. Indian tech and new-economy listings that trade on future growth feel the global discount-rate move whether or not their fundamentals have changed.

This is precisely where discipline should beat prediction. Nobody reading this — and nobody writing it — knows whether the Fed hikes twice, holds, or cuts. What operators can control is exposure. That means stress-testing budgets against a higher-for-longer scenario, being cautious about debt-funded expansion priced on cheap-capital assumptions, and not confusing a global liquidity tide with company-specific genius. For investors, it means accepting that a portfolio leaning hard into long-duration growth is, knowingly or not, a leveraged position on the rate path.

The AI revolution is real, and its long-term economics may well justify today’s ambitions. But this week’s volatility is a reminder that even transformative technology is priced through the lens of the discount rate — and that lens just got a lot less forgiving. The smart response is not to call the next Fed meeting. It is to build for a world where you cannot.