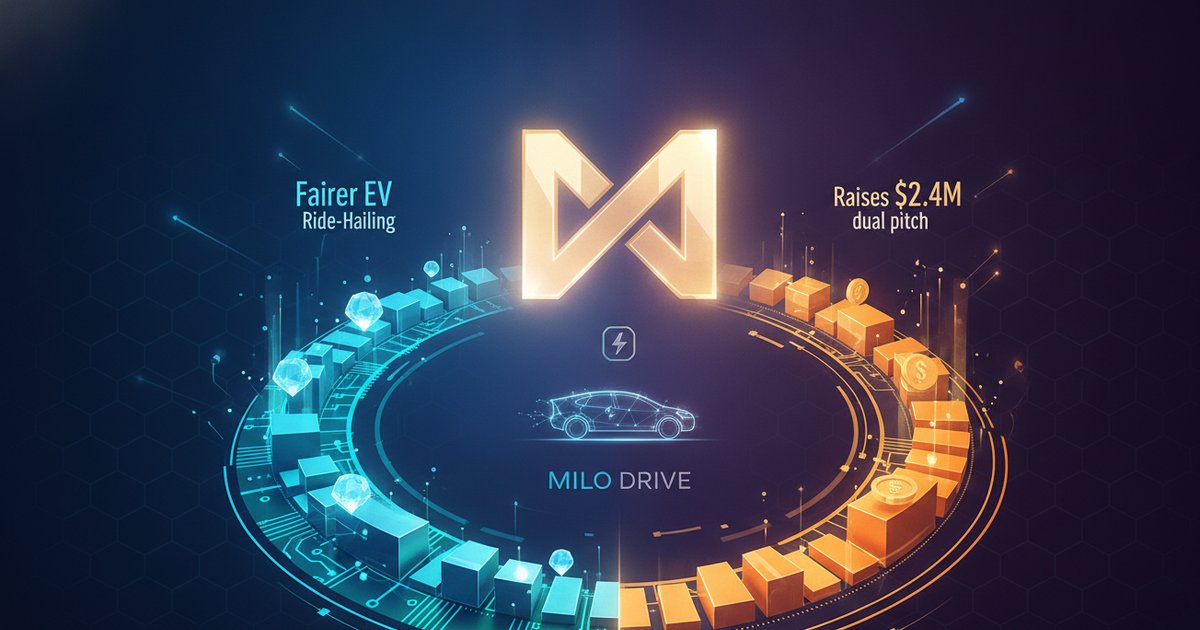

Every ride-hailing pitch of the last decade has promised to be better for someone: cheaper for riders, more flexible for drivers, or cleaner for cities. Rarely have those promises held together at once. Milo Drive, a Gurugram-based electric-mobility startup, is the latest to argue it can square the circle — cleaner electric rides and a fairer deal for the people behind the wheel — and it now has fresh capital to test that thesis.

The company said this week it has raised $2.4 million in seed funding to scale an asset-light EV ride-hailing platform, claiming more than a million rides to date and a roughly 20% lift in driver incomes. Those are the company’s own figures, and they sit at the centre of a larger, contested question: as ride-hailing electrifies, will the winners be the platforms that simply cut costs, or the ones that pair better unit economics with genuinely better terms for drivers?

The raise

Milo Drive raised $2.4 million (about ₹22.9 crore) in a seed round led by Caret Capital, according to reporting by Entrackr and Inc42. The round drew a notably deep bench of participating backers: Antler India (which some outlets describe as co-leading), Alteria Capital, IAN Capital, Climate Angels and Aureolis Capital, among others.

Founded in 2024 by Monil Jayeshkumar Khatri and Vishal Jewrajka, Milo Drive says it will use the money to accelerate EV adoption and, in its own words, “formalise” employment for India’s driver workforce — building out vehicle access, charging infrastructure, fleet-management tools and the technology layer that ties them together. In practice that means deepening its demand network, expanding the base of small fleet operators it works with, and sharpening the charging-intelligence software that keeps electric vehicles earning rather than idling.

It is a modest cheque by mobility standards — a sector where scaling fleets is capital-intensive — which is precisely why Milo Drive’s “asset-light” framing matters. Rather than owning vehicles outright, it positions itself as the operating system connecting drivers, fleet operators and ride demand, with the balance-sheet burden of the vehicles sitting elsewhere. Inc42 reports the company claims to have automated close to 90% of what would otherwise be manual fleet operations, a figure that speaks to where Milo Drive wants its edge to sit: in software and coordination rather than steel.

The presence of both a mobility-focused lead in Caret Capital and a climate-oriented syndicate — Climate Angels among them — signals the two audiences the company is courting at once. Antler India’s involvement, whether framed as co-lead or participant, reflects the early-stage, venture-studio pattern common to Indian mobility bets, where operational support often matters as much as the capital itself.

The dual pitch

Milo Drive’s story rests on two claims that it wants investors, drivers and riders to hear as one. The first is environmental: all-electric rides, in a country where transport is a major and rising source of urban air pollution. The second is social: better livelihoods for drivers, delivered through a driver app that the company says handles collections, charging guidance and earnings tracking.

The headline numbers, all company-reported: more than one million rides facilitated since launch, and a claimed ~20% increase in driver incomes attributed to its tools. Milo Drive frames the income gain as a product of transparency and efficiency — helping drivers see and manage their earnings, cut idle time, and route charging so vehicles spend more hours generating revenue.

Those are plausible mechanisms, but they are worth reading with a clear eye. A 20% income lift is a company metric, not an audited or independently verified figure, and it says nothing about the baseline it improves on or how it is measured. The direction of travel — toward more visible, better-managed driver earnings — is the genuinely interesting part; the precise magnitude deserves the caveats any founder-supplied number carries.

The hard market

The pitch is attractive. The market is brutal. Ride-hailing in India is dominated by well-capitalised incumbents, and a new “fairer to drivers” entrant has to win on economics that have humbled far larger players. Getting there means solving problems that are specific to electrifying a fleet, not just running one.

- Vehicle and charging economics. EVs shift cost from fuel to capital and charging time. Range limits, charging availability and battery health all bite into the hours a vehicle can earn — which is exactly why Milo Drive leans so hard on charging-intelligence and predictive maintenance as differentiators.

- The price-versus-pay squeeze. The central tension in any ride-hailing model is that riders want cheaper fares while drivers want higher pay, and the platform sits in between. Promising both cleaner rides and better driver incomes only works if electrification and software genuinely expand the pie, rather than shifting the same margin around.

- Incumbent gravity. Competing against established platforms means matching their density of demand and drivers, in city after city, before network effects tip in a challenger’s favour. That is a slow, expensive grind — and $2.4 million buys focus, not scale.

None of this is disqualifying. But it is the reason the driver-welfare pitch and the unit-economics pitch cannot be separated: a model that is kinder to drivers only survives if the underlying numbers work.

The India read

Zoom out, and Milo Drive is a small bet on a large shift. Shared mobility in India is electrifying, and the addressable prize is real if uncertain. Milo Drive cites market estimates that India’s EV ride-hailing segment could grow from about $0.24 billion in 2025 to roughly $4.2 billion by 2030 — a headline ~77% CAGR, per figures the company points to. Treat that as a directional signal rather than gospel: it is a company-cited projection, and third-party EV forecasts vary widely in their assumptions.

The more durable story is the one about work. India’s gig economy has become a live policy and public debate, and “formalising” driver employment is a loaded phrase — it can mean better benefits and stability, or simply tighter platform control, depending on how it is implemented. Better earnings transparency and lower idle time are correlated with better driver outcomes, but correlation is not a promise; the association between slick driver tooling and genuinely improved livelihoods is real, not automatic, and worth watching rather than assuming.

There is also a supply-side logic worth naming. Small fleet operators and individual driver-entrepreneurs are the connective tissue of Indian shared mobility, and a platform that lowers the friction of running an electric vehicle — access, charging, maintenance, collections — is effectively selling them a business-in-a-box. If that tooling genuinely raises take-home pay, it becomes a recruitment and retention advantage against incumbents in a market where driver churn is a chronic cost. That is the most credible version of Milo Drive’s “fairer to drivers” claim: not charity, but a flywheel where better driver economics feed better supply, which feeds better service.

For founders and operators, the useful takeaway is less about Milo Drive specifically and more about the pattern it represents. As electrification reshapes mobility, the companies most likely to endure will be those that treat driver economics as a core part of the product, not a marketing layer over it. Milo Drive has made that bet explicit. Whether the numbers — the rides, the income lift, the market — hold up under scale is the story to follow, not the seed round itself.