The story of an early-stage funding slowdown is, by now, a familiar one. Investors have grown cautious, cheques have shrunk, and founders have learned to do more with less. But fresh data out of Canada gives that narrative an unusually blunt edge: not only is there less money flowing into the riskiest, earliest part of the market, there are also fewer founders raising it at all — while the cost of building remains stubbornly unchanged.

That combination — fewer companies, thinner capital, steady costs — is the precise shape of an early-stage squeeze. It’s worth examining closely, both because Canada’s pre-seed and seed market is a clean test case for a broader global trend, and because India’s own founders and funders should read it as a warning rather than a far-off curiosity.

The data

According to RBCx data published on June 24, 2026, both the number of Canadian companies raising venture capital and the total amount raised fell roughly 40% year over year in the first quarter of 2026. That isn’t a soft quarter; it’s a structural contraction. And it wasn’t a slow drift, either: Q1 2026 was down around 31% from Q4 2025, suggesting the decline accelerated into the start of the year rather than bottoming out.

The most telling detail sits inside that headline number. Even as the overall pool shrank, the average seed round held steady at about $3 million, per RBCx. In other words, the price of getting a company off the ground didn’t fall to match the smaller pool of capital. Founders who managed to raise still needed roughly the same amount they always did — because salaries, cloud bills, lab equipment, and runway don’t discount themselves just because the market has cooled.

What that produces is concentration. When the total capital available drops sharply but individual round sizes stay flat, the math forces a brutal narrowing: capital pools around fewer companies. The founders who clear the bar get funded at familiar levels; everyone else gets nothing. The middle thins out. A market that should be widening at its base — the pre-seed and seed layer is meant to be a broad funnel — is instead pinching shut at exactly the point where breadth matters most.

Why it bites

An early-stage contraction hurts more in some economies than others, and Canada is unusually exposed. RBCx notes that deeptech sectors — cleantech and life sciences in particular — remain heavily reliant on venture funding. These are not businesses that can bootstrap their way through a dry spell on early revenue. They require years of capital-intensive R&D before a product, let alone a customer, exists. Venture money isn’t a nice-to-have for them; it’s the oxygen supply.

That dependence is precisely why a sustained early-stage decline is more dangerous than a one-off bad quarter. When seed capital dries up for a cleantech or biotech founder, the company doesn’t just slow down — it often never starts. And the projects that die quietly at the napkin stage are invisible in the data. You can count the rounds that didn’t happen; you can’t count the companies that were never incorporated because the founder did the math and walked away.

The deeper risk, then, is to the innovation pipeline itself. A healthy early-stage ecosystem is a numbers game: fund many bets, accept that most fail, and let the rare winners carry the returns and the breakthroughs. Shrink the number of bets by 40% and you don’t just lose 40% of the outcomes — you lose disproportionately, because the next category-defining company is statistically more likely to come from a wide funnel than a narrow one. Fewer founders entering the market today means fewer scaleups in five years and fewer anchor companies in ten. The damage compounds slowly and shows up late, which is exactly what makes it easy to ignore until it’s irreversible.

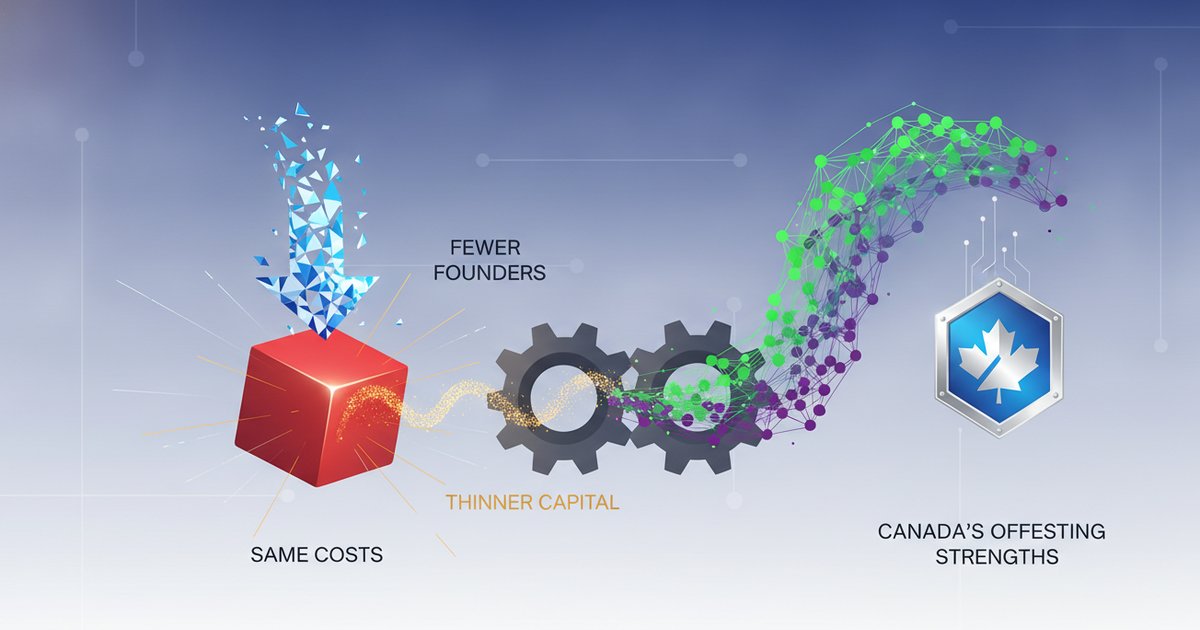

Canada’s offsetting strengths

None of this means Canada is sliding off a cliff. The early-stage crunch is real, but it lands on an ecosystem with genuine structural advantages that soften the blow.

The most durable is policy. Canada’s R&D tax credit regime gives capital-intensive startups a way to stretch each dollar — effectively subsidising the expensive experimentation that deeptech and life sciences depend on. When venture money is scarce, a credit that returns a meaningful share of R&D spend functions as a kind of non-dilutive backstop, letting founders keep building through a fundraising winter.

The second is talent. Canada’s immigration pipeline has been a quiet competitive weapon, drawing engineers and researchers who might otherwise have defaulted to Silicon Valley. A steady inflow of skilled founders and operators is the raw material of any ecosystem, and it’s one thing a capital crunch can’t immediately erode.

The third is cost discipline by default. Canadian startups have long run leaner than their counterparts in San Francisco or New York — lower salaries, lower overheads, more conservative burn. In a flush market that looks like a disadvantage. In a squeeze, it’s survival armour: a company that never built a bloated cost base has less to cut and more runway per dollar raised.

Layered on top is an unusually active set of government and bank-led support structures — including, notably, the kind of institutional backing represented by an RBCx itself publishing this data. When public and strategic capital steps in to steady the early stage, it can blunt the worst of a private-market pullback. None of these offsets reverse the 40% drop. But together they explain why Canada can absorb a shock that might break a thinner ecosystem.

The India read

For Indian founders and investors, the temptation is to file this under “someone else’s problem.” That would be a mistake, because India carries a version of the same structural vulnerability — arguably a more pronounced one.

India’s funding market has long skewed toward later stages. The headlines, the mega-rounds, the unicorn announcements cluster around growth and pre-IPO capital, while the earliest layer — the messy, unglamorous pre-seed and seed tier — gets comparatively less attention and, in tough cycles, less money. That imbalance is the same fault line Canada is now feeling, just expressed differently. When global sentiment tightens, it’s the early stage that gets cut first and deepest, because it’s where the risk is highest and the proof is thinnest.

The first lesson is about the role of public and strategic capital. Canada’s offsets — R&D credits, government and bank-led programmes — show what it looks like when non-dilutive and institutional money is built into the system to catch the early stage when private VC retreats. India has its own instruments here, from government-backed funds to startup-focused schemes, but the Canadian data is a reminder that these are not bureaucratic box-ticking exercises. In a downturn, they are the difference between a funnel that narrows and one that collapses. The case for strengthening that scaffolding is strongest precisely when the private market is weakest.

The second lesson is for founders, and it’s simpler: discipline is the survival skill. The Canadian story is, at its core, about steady costs meeting shrinking capital. The founders who endure that math are the ones who never assumed cheap money would keep flowing — who kept burn low, runway long, and the gap between fundraises survivable. Indian founders who internalised the lessons of 2022 and 2023 already know this. The Canadian numbers are confirmation that the discipline isn’t a phase to wait out; it’s the new baseline.

The pattern is global. Canada just shows it in sharper relief: fewer founders, the same costs, thinner capital. The economies that come through it intact won’t be the ones that wished the money back — they’ll be the ones that built scaffolding underneath their earliest founders and ran lean enough to outlast the squeeze. That’s the read India should take, while there’s still time to act on it.