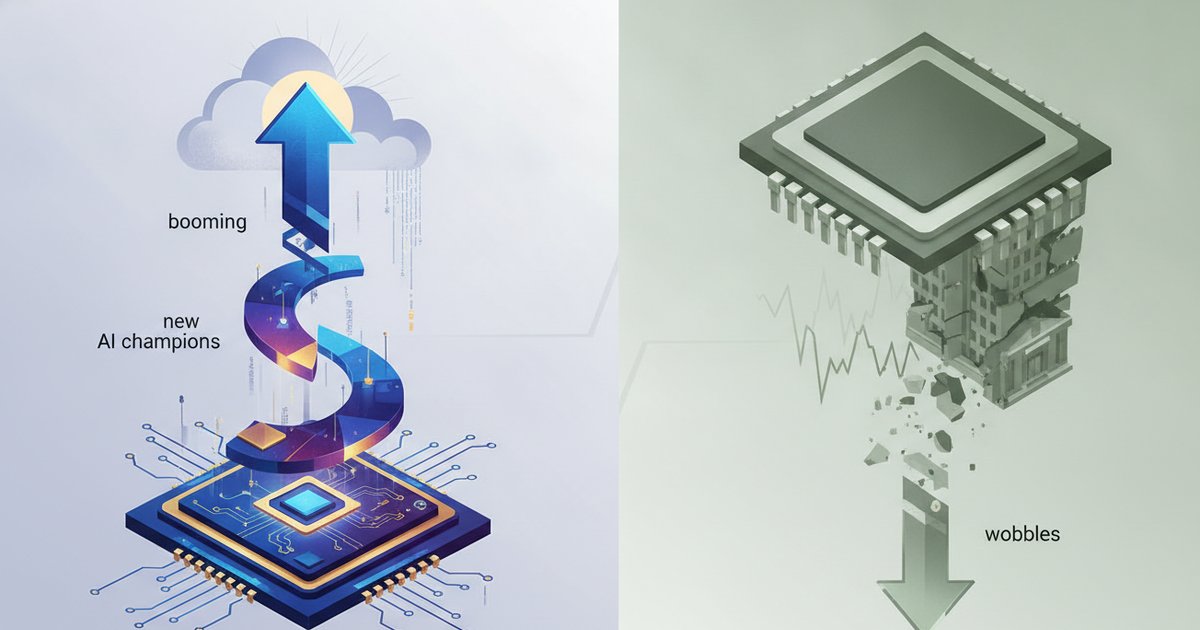

This week handed investors a split screen. On one side, US semiconductor names took a beating as Wall Street openly questioned whether the torrent of AI capital expenditure will ever pay off. On the other, a clutch of Chinese AI-chip companies kept marching higher, posting maiden profits, triple-digit revenue growth and a blockbuster Hong Kong listing. Two semiconductor stories, moving in opposite directions, at the same moment. The gap is worth reading carefully — not because one market is right and the other wrong, but because the two are pricing fundamentally different things.

A tale of two chip markets

The US side of the ledger was ugly. Micron slid roughly 13% and the closely watched PHLX Semiconductor index dropped about 7.9% as doubts hardened over the returns on AI capital expenditure, according to CBS News citing Reuters. The selling reflected a question that has been simmering for months and finally boiled over: if hyperscalers are pouring tens of billions into GPUs and data centres, where is the corresponding revenue, and how long until depreciation starts eating into the AI-trade thesis that has carried these stocks?

Meanwhile, China’s domestic chip champions were doing the opposite. Cambricon, Moore Threads and Biren have been rallying on public markets even as their American counterparts wobbled. The contrast is stark — and it is not a coincidence of timing so much as a difference in what each market is betting on.

The drivers diverge as much as the price action. US chip valuations are tethered to a global, return-on-investment narrative: will enterprises and cloud providers extract enough productivity and revenue from AI to justify the spend? China’s domestic chip stocks are riding a more localised, policy-shaped story — one about self-sufficiency, captive demand and a national imperative that is far less sensitive to near-term ROI math. Different investors, too: the China names trade heavily on mainland and Hong Kong exchanges, where retail enthusiasm and strategic-sector sentiment carry weight that a Nasdaq quant desk would discount.

China’s new champions

The numbers behind the rally are eye-catching. According to EEWorld, citing AspenCore’s 2026 AI Chip TOP10 list, Cambricon reached a market capitalisation near ¥443 billion on the back of its first annual profit, with FY25 revenue of roughly ¥6.5 billion. For a company that spent years burning cash to build a domestic alternative to foreign accelerators, crossing into profitability is a symbolic milestone as much as a financial one — proof that the import-substitution model can, eventually, generate a business.

Moore Threads, a younger GPU-focused contender, posted around 243% revenue growth in 2025 per the same source. That kind of expansion off a small base is what momentum investors live for, and it signals that demand for home-grown accelerators is real and accelerating, not theoretical.

Then there is Biren, whose Hong Kong debut in January 2026 jumped roughly 120% on day one, again per EEWorld citing AspenCore. A first-day pop of that magnitude tells you two things: appetite for Chinese AI-silicon exposure is intense, and public-market capital is now flowing toward a sector that was, until recently, the preserve of state funds and strategic investors. (These figures are point-in-time and worth treating as snapshots rather than steady-state valuations.)

Taken together, the three companies sketch a maturing ecosystem: an incumbent reaching profitability, a fast-grower scaling revenue, and a newcomer tapping public markets. That is the shape of an industry finding its feet, not a single speculative bubble.

What’s really being priced

Strip away the daily price moves and the China rally is pricing one dominant variable: import substitution under export controls. Washington’s restrictions on advanced AI accelerators reaching China have done something no industrial policy memo could engineer on its own — they have created a guaranteed, policy-protected market for domestic alternatives. When the best foreign chips are hard to buy, the second-best local chip becomes the only chip, and its maker gets a customer base by default.

That feeds the second factor: a captive domestic demand base. China’s cloud providers, AI labs and state-linked enterprises need compute, and increasingly they need compute that is procurement-safe regardless of how the geopolitical weather turns. For a domestic chipmaker, that is the closest thing to a structural moat — demand that exists not because your product is the global best, but because your product is the available and politically durable one.

But there is a lingering qualifier that the bull case tends to underweight, and it is the one that separates a hardware win from a platform win: the software-ecosystem gap. Nvidia’s enduring advantage was never purely silicon; it was CUDA and the decade-plus of libraries, tooling and developer habit built on top of it. Chinese chipmakers can match or approach raw hardware specs faster than they can replicate that software gravity. Migrating models, retraining engineers and rebuilding toolchains is slow, expensive work. Until the domestic software stack is genuinely sticky, the moat is part hardware, part policy — and policy moats can shift. That is the unpriced risk beneath the surging valuations, and investors buying the momentum should hold it in view.

The India read

For Indian readers — founders, fund managers and policymakers alike — the divergence carries several lessons that are easy to miss amid the share-price drama.

First, on chip-stock and fab ambitions: China’s experience shows that domestic semiconductor champions can be willed into existence, but the catalyst was a combination of sustained state demand, patient capital and external pressure that created a protected market. India’s fab push and its emerging electronics-and-semiconductor ecosystem can learn from the demand-side discipline. Subsidising fabs without engineering anchor customers risks building capacity that no one is contractually obliged to fill. The China model worked partly because the buyers were already lined up — by policy, by necessity, or both.

- Demand certainty matters more than headline incentives. A captive buyer base did more for Cambricon than any single subsidy line.

- Software is the long game. India’s strength in software talent could, in theory, be an advantage in building accelerator toolchains — but only if it is deliberately funded alongside hardware, not treated as an afterthought.

- Public-market readiness signals maturity. Biren’s Hong Kong debut shows that a deep-tech chip sector can eventually attract listing capital. India’s deep-tech IPO pipeline is thinner, and closing that gap requires companies with real revenue, not just roadmaps.

Second, the broader strategic point: a maturing China chip sector means the global compute supply is diversifying, whether the West likes it or not. For India, sitting between competing technology blocs, that diversification is an opportunity. A world with multiple credible accelerator ecosystems gives Indian buyers — from cloud firms to AI startups — more negotiating leverage and more sourcing options, even if today the practical choice for frontier work still runs through US silicon.

Finally, the global signal. The US sell-off and the China rally are not contradictory; they are two halves of the same transition. The American market is repricing the returns on AI infrastructure, while the Chinese market is pricing the strategic necessity of building it domestically. One is a question about profit. The other is a question about sovereignty. Both will shape where compute is made, who controls it, and what it costs — and that is a story India cannot afford to watch from the sidelines.

This feature combines reporting on point-in-time market figures with editorial analysis; valuations and growth rates cited are snapshots and should be verified against current data before any investment decision.